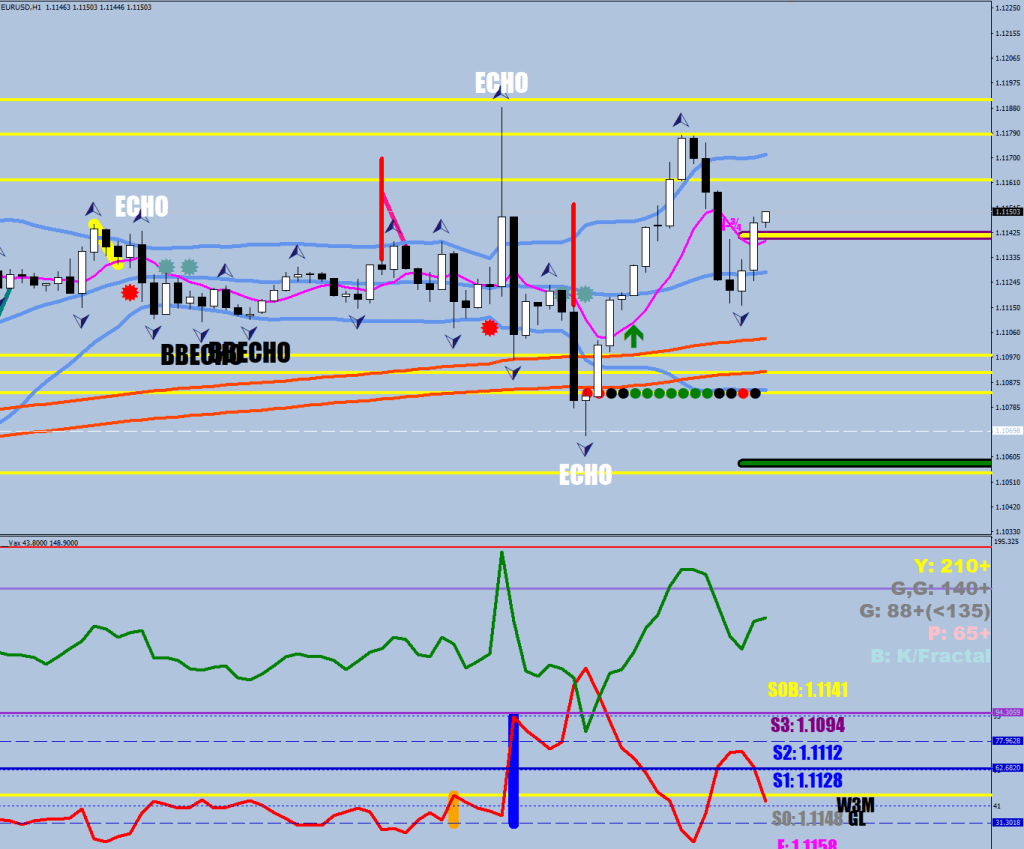

This market has not failed the upside yet (Echo).

Them schmucks are still long.

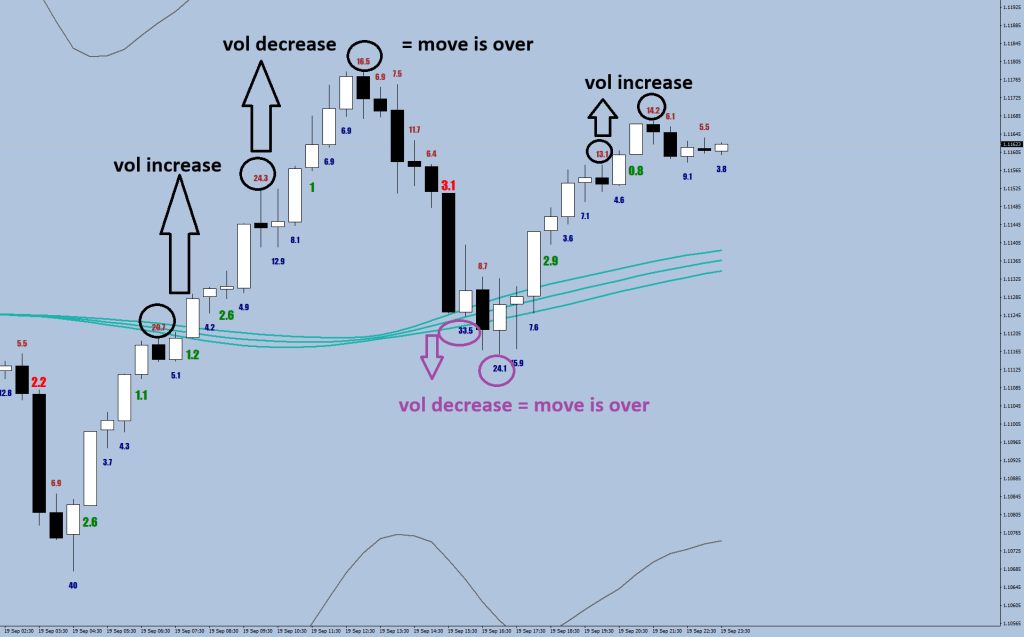

Now, how would I go about compressing counter-directional volatility, if I had to write a routine for it?

I cannot see the order flow, but here’s what I think.

If they want the market to turn back up every time it has gone 10 pips away from the most recent 30-minute high, I would put out orders with some gap between and in increasing volume.

For instance, for 9 hours (18 candles) the program gets turned on, that says: buy X lots 6 pips out, buy 2x lots 8 pips out, buy 4x lots 10 pips out, and put out an 8x order 12 pips out.

Above the strongest 9-hour compression ever. 12.5 pips was the maximum counter-directional move.

Of course, you cannot do this indefinitely and you must dump your collection onto a larger order area. Say where someone got trapped and has their stop at break-even or where they have trailed their stop loss to.

Now, the flip side of volatility compression, is that when the market breaches, there will be no stopping in the other direction for some time. I.e. the correction went to an RSI2 below 5 reading.

Album #25 as promised.

deletetxt1("Citera");

if (Period()==30){

for (i=lookback; i>=0; i--){

if (Open[i]<Close[i] || Open[i+1]<Open[i+1]) {

ObjectCreate("Citera"+IntegerToString(i), OBJ_TEXT, 0, Time[i], Low[i]-20*Point);

ObjectSetText("Citera"+IntegerToString(i), NormalizeDouble((iHigh(symbol,0,iHighest(symbol,0,MODE_HIGH,2,i+1))-Low[i])*10000,2), 11, "Impact", Navy);

}

}

}