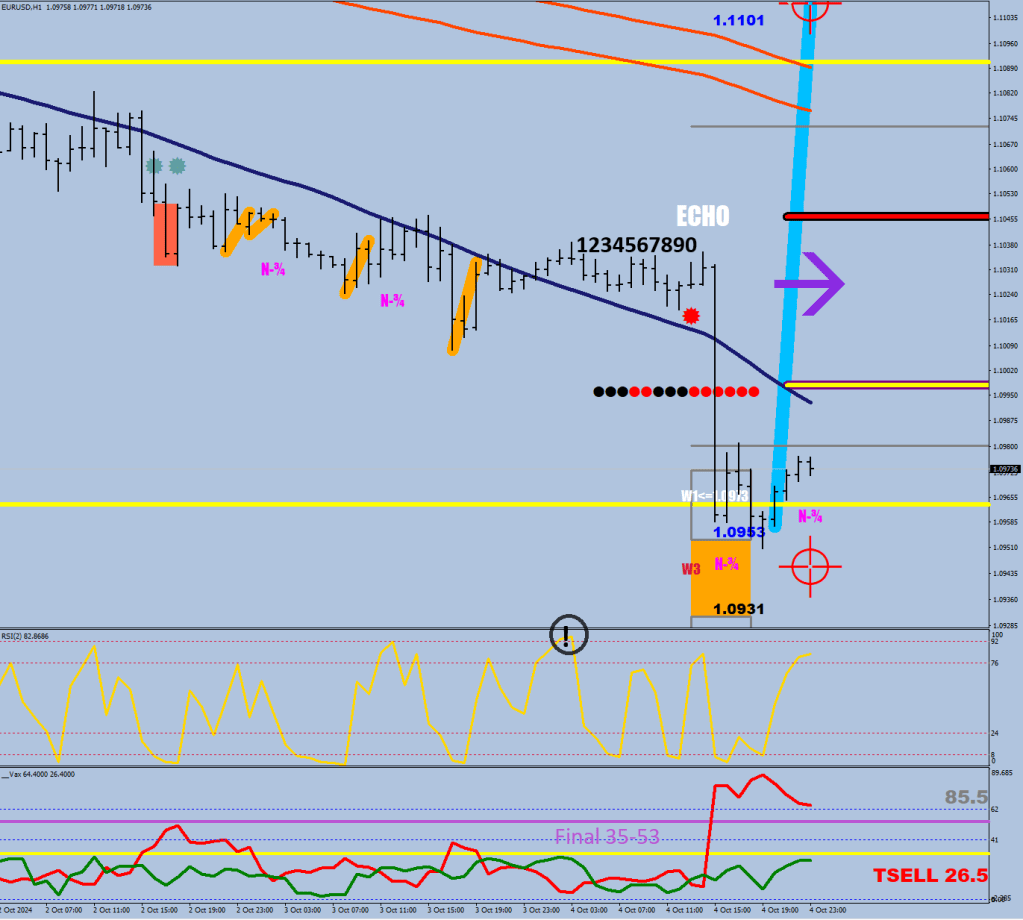

There goes the capitulation. 10 hours+ without RSI2 greater than 92.

On the 12th hour NFP.

ObjectCreate("PENELOPED"+6,OBJ_LABEL,2, 0,0);

ObjectSet("PENELOPED"+6,OBJPROP_CORNER,1);

ObjectSet("PENELOPED"+6,OBJPROP_XDISTANCE,0);

ObjectSet("PENELOPED"+6,OBJPROP_YDISTANCE,20);

ObjectSet("PENELOPED"+6,OBJPROP_COLOR,clrGray);

ObjectSetText("PENELOPED"+6, DoubleToStr(NormalizeDouble(ExtATRBuffer[ArrayMaximum(ExtATRBuffer,10,0)],2),1),19,"Arial Black");

if (ExtATRBuffer[ArrayMaximum(ExtATRBuffer,10,0)]<35 && RSI2[ArrayMaximum(RSI2,10,0)]>8) {ObjectSetText("PENELOPED"+6,"TBUY "+DoubleToStr(NormalizeDouble(ExtATRBuffer2[ArrayMaximum(ExtATRBuffer2,10,0)],2),1),19,"Arial Black");

ObjectSet("PENELOPED"+6,OBJPROP_COLOR,clrGreen);

}

ObjectCreate("PENELOPED"+9,OBJ_LABEL,2, 0,0);

ObjectSet("PENELOPED"+9,OBJPROP_CORNER,3);

ObjectSet("PENELOPED"+9,OBJPROP_XDISTANCE,0);

ObjectSet("PENELOPED"+9,OBJPROP_YDISTANCE,20);

ObjectSet("PENELOPED"+9,OBJPROP_COLOR,clrGray);

ObjectSetText("PENELOPED"+9,DoubleToStr(NormalizeDouble(ExtATRBuffer2[ArrayMaximum(ExtATRBuffer2,10,0)],2),1),19,"Arial Black");

if (ExtATRBuffer2[ArrayMaximum(ExtATRBuffer2,10,0)]<35 && RSI2[ArrayMaximum(RSI2,10,0)]<92) {ObjectSetText("PENELOPED"+9,"TSELL "+DoubleToStr(NormalizeDouble(ExtATRBuffer2[ArrayMaximum(ExtATRBuffer2,10,0)],2),1),19,"Arial Black");

ObjectSet("PENELOPED"+9,OBJPROP_COLOR,clrRed);

}Which leaves us with what?

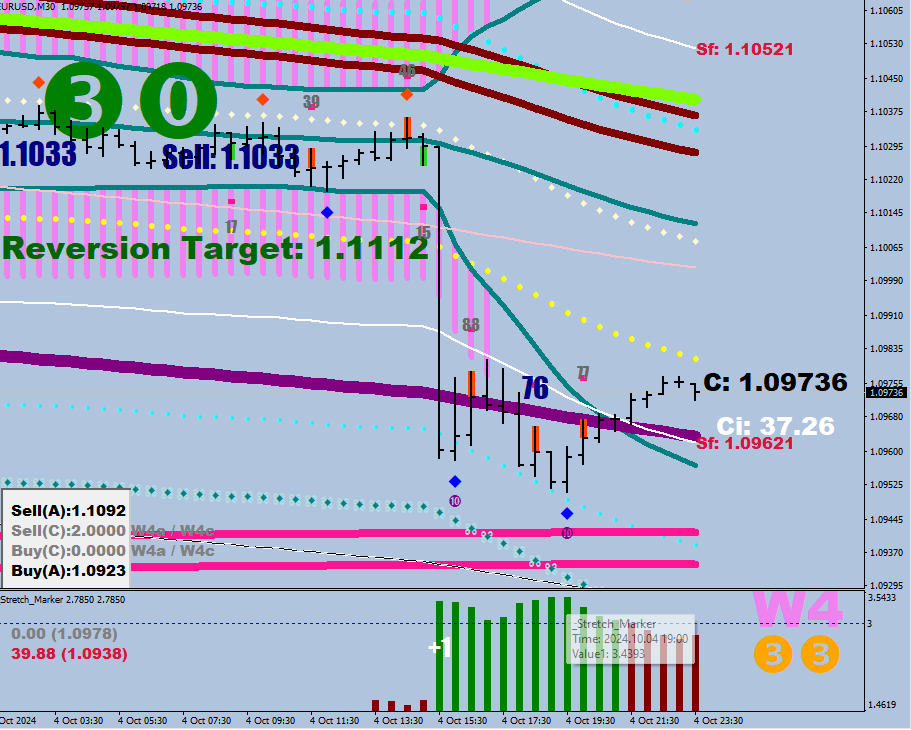

All systems go would be CF1 and CF2 of the same color and Trending Sell / Trending Buy approval from Vax.

CF1 has not changed, until an ECHO or a BBECHO print on the downside, this remains RED. In fact, a fresh ECHO print was made in the hour before the NFP reinforcing the signal.

CF2 has finally changed, it is now red with absolute volatility expansion breaches at over 49.

For the first time since the 1.12 top.

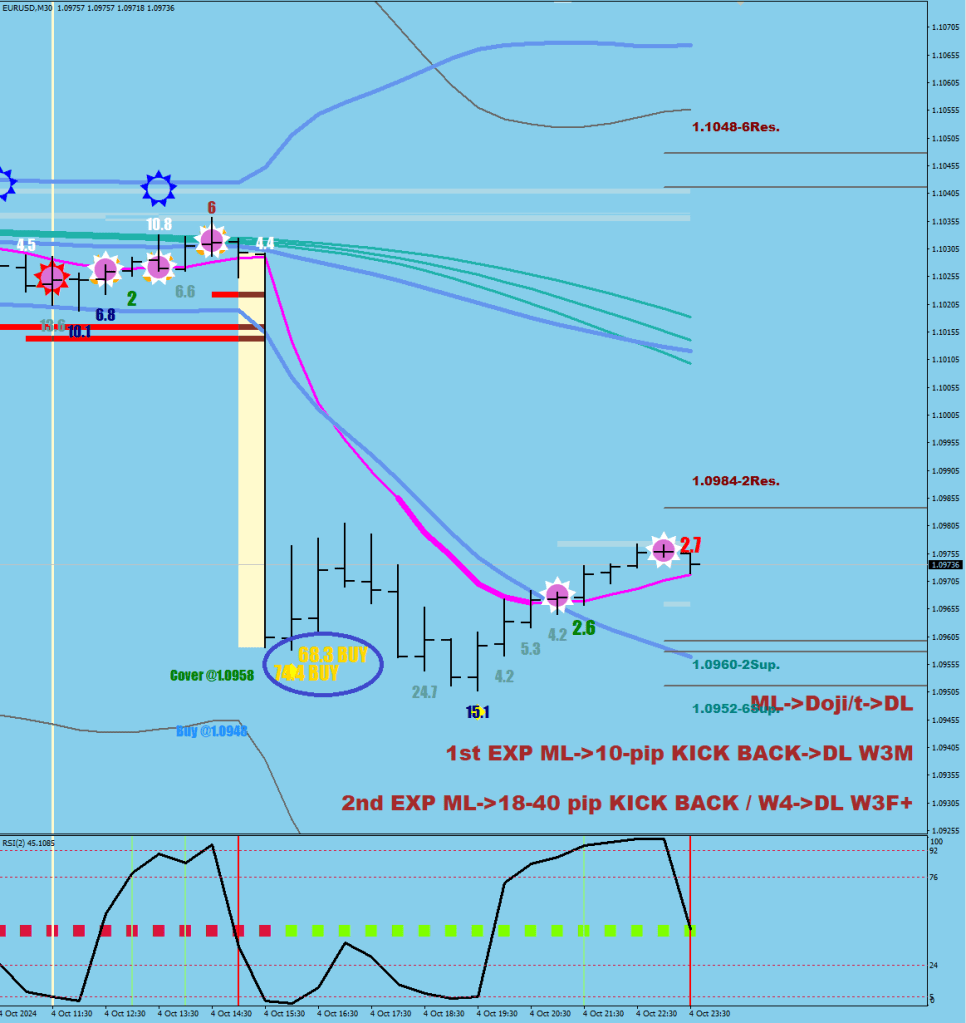

There is a gray volatility compression divergence,

They have utilized the Money Flow reversal zone’s breakout option.

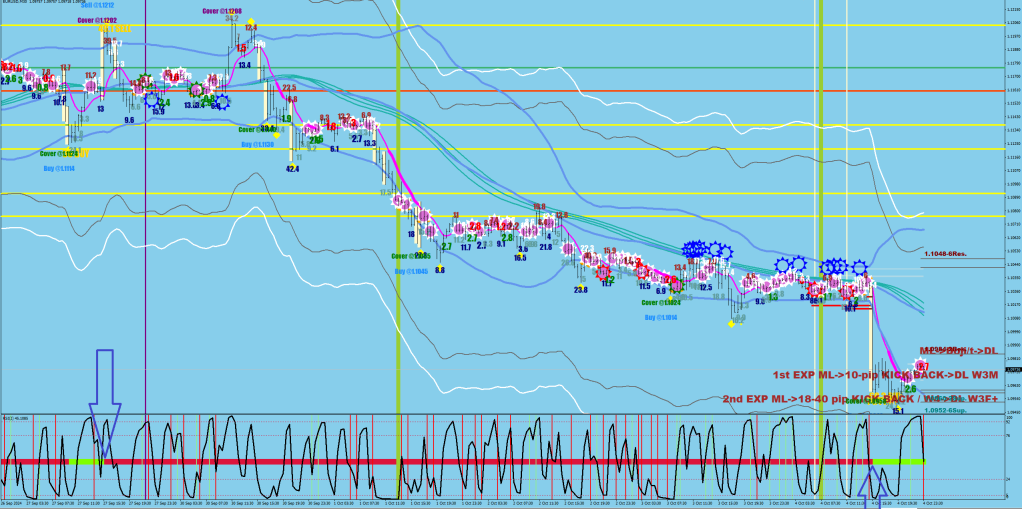

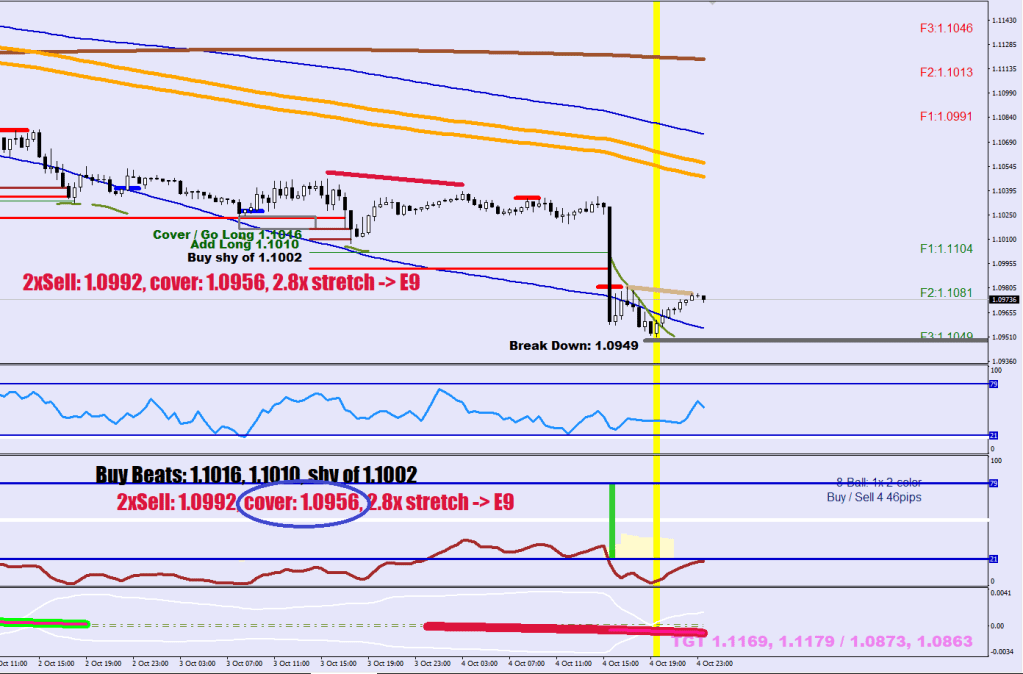

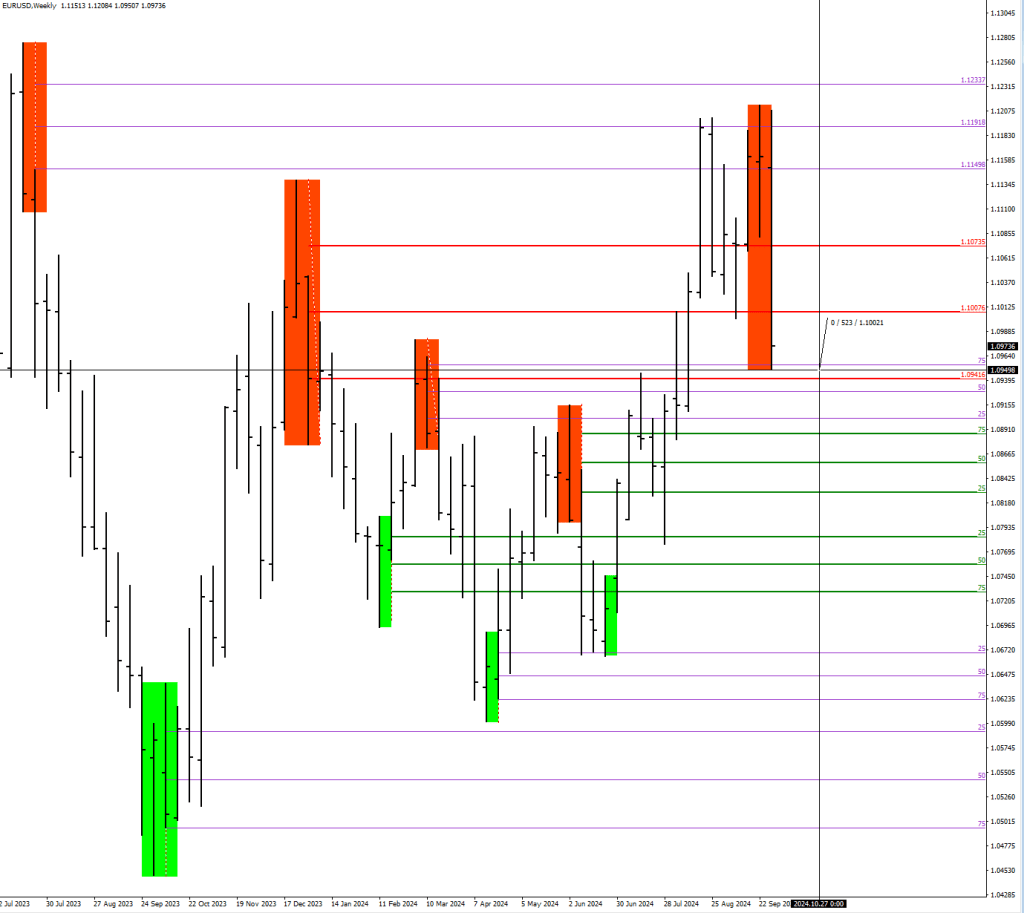

A 3.49x stretch was achieved, which could trigger a mean reversion to the daily E-9. It is going to be at around 1.1060 on Monday, moving about 20 pips a day lower. The bear’s game would be not letting the mean reversion play out by shorting about 40 pips lower than the E9 of Lows.

The Swing High has finally been printed, and a continuation could come 40-56 higher than this week’s low (typically 53/56 pips) which would put the price back at 1.10 at some point.

One last remark is that the daily stochastic reading is too high for today to be the swing low. It was at 13.6 and the optimal range to hit is 8.5 to 4, but of course, this Oscillator is bound to move lower, but typically a lower low is in the cards before a move back up.

1.1008-1.1017 is the optimal zone for a bear to reload.

In the meantime, I made a Synth album to listen to.