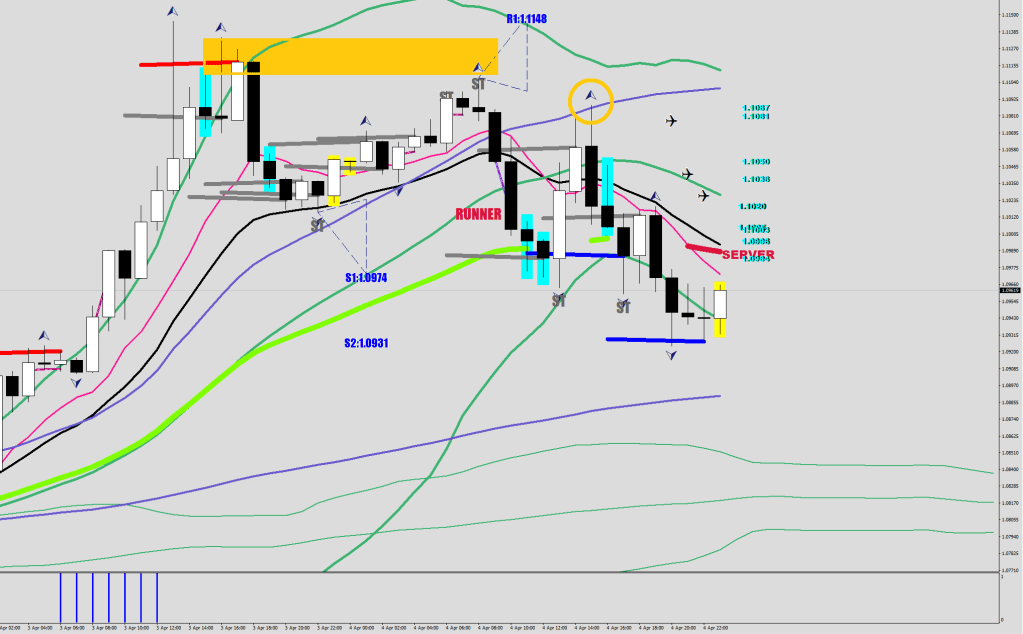

So, the primary exit was about the pro volume candle’s high, and once this condition was met, the secondary exit at the 120-sample BB. Both highlighted with an orange marker.

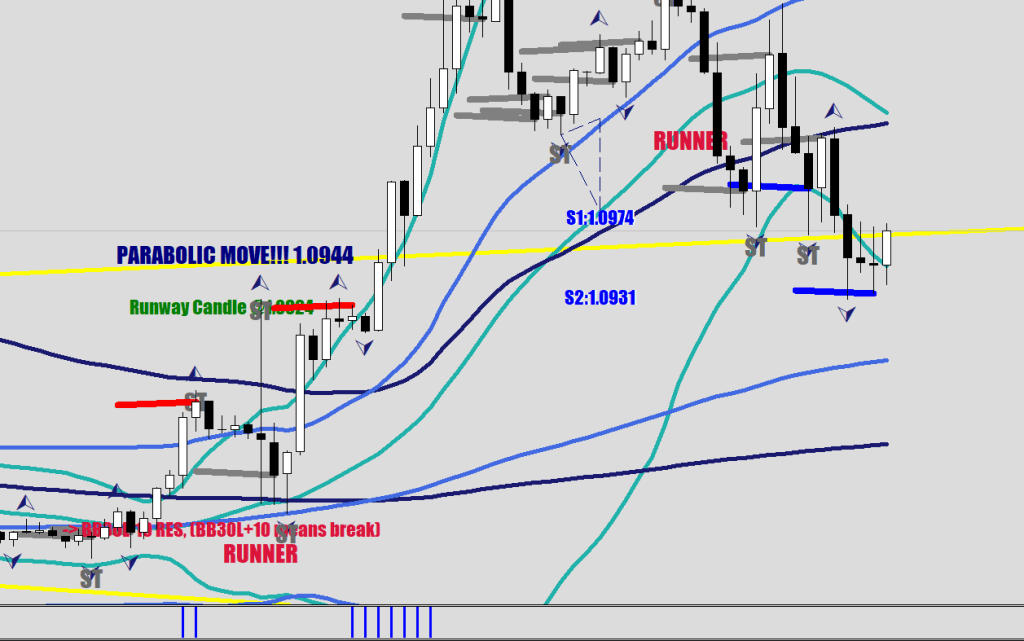

Now, let’s figure out some filters for the parabolic move in real time.

///parabolic break up

if ((High[i+3]>High[i+4] || High[i+4]>High[i+5])

&& Close[i+3]>iBands(symbol,0,30,2,0,PRICE_MEDIAN,MODE_UPPER,i+3)

&& High[i+1]-Low[i+1]<900*Point

&& (High[i+2]-Low[i+2]>400*Point || (Close[i+4]>iBands(symbol,0,30,2,0,PRICE_MEDIAN,MODE_UPPER,i+4) && Close[i+5]>iBands(symbol,0,30,2,0,PRICE_MEDIAN,MODE_UPPER,i+5)))

&& High[i+2]<High[i+3] && Close[i+2]<iBands(symbol,0,30,2,0,PRICE_MEDIAN,MODE_UPPER,i+2)

&& Close[i+1]>iBands(symbol,0,30,2,0,PRICE_MEDIAN,MODE_UPPER,i+1) && High[i+1]==iHigh(symbol,0,iHighest(symbol,0,MODE_HIGH,4,i+1))

&& High[i+1]>iBands(symbol,0,120,2,0,PRICE_MEDIAN,MODE_UPPER,i+1)

)

{

ObjectCreate("Bitera"+IntegerToString(i), OBJ_TEXT, 0, Time[i+12], High[i+1]+50*Point);

ObjectSetText("Bitera"+IntegerToString(i), "PARABOLIC MOVE!!! "+DoubleToStr(NormalizeDouble(Close[i+1],4),4) , 21, "Impact", Navy);

}

///parabolic break down

if ((Low[i+3]<Low[i+4] || Low[i+4]<Low[i+5])

&& Close[i+3]<iBands(symbol,0,30,2,0,PRICE_MEDIAN,MODE_LOWER,i+3)

&& High[i+1]-Low[i+1]<900*Point

&& (High[i+3]-Low[i+3]>400*Point || (Close[i+4]<iBands(symbol,0,30,2,0,PRICE_MEDIAN,MODE_LOWER,i+4) && Close[i+5]<iBands(symbol,0,30,2,0,PRICE_MEDIAN,MODE_LOWER,i+5)))

&& Low[i+2]>Low[i+3] && Close[i+2]>iBands(symbol,0,30,2,0,PRICE_MEDIAN,MODE_LOWER,i+2)

&& Close[i+1]<iBands(symbol,0,30,2,0,PRICE_MEDIAN,MODE_LOWER,i+1)+20*Point

&& Low[i+1]<=iLow(symbol,0,iLowest(symbol,0,MODE_LOW,4,i+1))+20*Point

&& Low[i+1]<iBands(symbol,0,120,2,0,PRICE_MEDIAN,MODE_LOWER,i+1)

)

{

ObjectCreate("Bitera"+IntegerToString(i), OBJ_TEXT, 0, Time[i+12], Low[i+1]-30*Point);

ObjectSetText("Bitera"+IntegerToString(i), "PARABOLIC MOVE!!! "+DoubleToStr(NormalizeDouble(Close[i+1],4),4) , 21, "Impact", Navy);

}One common denominator is that things can go awry beyond the 120-sample BB. The exit condition would be an FFF++ distance (end of the Pendulum) unless the price is already outside of it. The first example was something that went outside and never cared to consolidate, so I had to find usable conditions with an unknown playfield.

Let’s write an overhedger that would put you in a 20% extra directional holding even if you are asleep.

// Parabolic Overhedger by Macdulio

#include <stdlib.mqh>

extern double Equity = 400;

extern int magic_number = 98;

extern int magic_number2 = 99;

extern double Ratio = .6;

extern double overhedge = 120;

extern double MarginCallPercentage = 100;

extern double FSize=32;

#property copyright "by Macdulio in 2025"

#property link "https://forexfore.blog"

#property description "Parabolic Overhedger"

int profits;

double nakedshorts[];

double nakedlongs[];

double open_price;

double stop_loss_price;

double take_profit_price;

double open_price2;

double stop_loss_price2;

double take_profit_price2;

double OrderOpenPrice;

double OrderProfit;

string symbol = Symbol();

int init() {

return(0);

}

int deinit() {

return(0);

}

int start() {

int i, counter;

int counted_bars=IndicatorCounted();

int longcount, shortcount;

double nlongs;

double nshorts;

double longaveragebuffer;

double shortaveragebuffer;

int order_type;

profits = 0;

int hstTotal=OrdersHistoryTotal();

counter = 0;

// Print("Ratio = ", Ratio);

for(i=OrdersTotal()-1; i>=0 ; i--)

{

if(OrderSelect(i,SELECT_BY_POS,MODE_TRADES)==false)

{

Print("Access to orders list failed with error (",GetLastError(),")");

break;

}

if (OrderType() == OP_BUY)

{

nlongs = nlongs+OrderLots();

longcount = longcount+1;

longaveragebuffer = longaveragebuffer+(OrderOpenPrice()*OrderLots());

}

if (OrderType() == OP_SELL )

{

nshorts = nshorts+OrderLots();

shortcount = shortcount+1;

shortaveragebuffer = shortaveragebuffer+(OrderOpenPrice()*OrderLots());

}

}

if (nlongs!=nshorts){

// Parabolic break up OverHedge for shorts

if (nlongs<nshorts && (High[3]>High[4] || High[4]>High[5])

&& Close[3]>iBands(symbol,0,30,2,0,PRICE_MEDIAN,MODE_UPPER,3)

&& High[1]-Low[1]<900*Point

&& (High[2]-Low[2]>400*Point || (Close[4]>iBands(symbol,0,30,2,0,PRICE_MEDIAN,MODE_UPPER,4) && Close[5]>iBands(symbol,0,30,2,0,PRICE_MEDIAN,MODE_UPPER,5)))

&& High[2]<High[3] && Close[2]<iBands(symbol,0,30,2,0,PRICE_MEDIAN,MODE_UPPER,2)

&& Close[1]>iBands(symbol,0,30,2,0,PRICE_MEDIAN,MODE_UPPER,1) && High[1]==iHigh(symbol,0,iHighest(symbol,0,MODE_HIGH,4,1))

&& High[1]>iBands(symbol,0,120,2,0,PRICE_MEDIAN,MODE_UPPER,1)

) {

RemoveStopsandTargets();

open_price2 = NormalizeDouble(Ask, Digits);

stop_loss_price2 = NormalizeDouble(0.00,Digits);

take_profit_price2 = NormalizeDouble(0,Digits);

for (i = OrdersTotal() - 1; i >= 0; i--)

if (OrderSelect(i, SELECT_BY_POS))

if (OrderMagicNumber() == magic_number2) {

order_type = OrderType();

if (order_type == ORDER_TYPE_BUY) {

if ((NormalizeDouble(OrderOpenPrice(), Digits) != open_price2) || (NormalizeDouble(OrderStopLoss(), Digits) != stop_loss_price2) || (NormalizeDouble(OrderTakeProfit(), Digits) != take_profit_price2)) {

if (!OrderModify(OrderTicket(), open_price2, stop_loss_price2, take_profit_price2, OrderExpiration()))

Print("Error: ", ErrorDescription(_LastError));

}

break;

}

else if (order_type == ORDER_TYPE_BUY)

break;

}

if (i < 0)

if (OrderSend(symbol, OP_BUY, NormalizeDouble((nshorts-nlongs)*overhedge/100,2), open_price2, 3, stop_loss_price2, take_profit_price2, magic_number2+" EQUITY HEDGER BUY 0/0", magic_number2) < 0)

Print("Error: ", ErrorDescription(_LastError));

}

else

for (i = OrdersTotal() - 1; i >= 0; i--)

if (OrderSelect(i, SELECT_BY_POS))

if (OrderMagicNumber() == magic_number2 )

if (OrderType() == ORDER_TYPE_BUY_STOP)

if (!OrderDelete(OrderTicket()))

Print("Error: ", ErrorDescription(_LastError));

// Parabolic break down OverHedge For Longs

if (nshorts<nlongs && (Low[3]<Low[4] || Low[4]<Low[5])

&& Close[i]<iBands(symbol,0,30,2,0,PRICE_MEDIAN,MODE_LOWER,3)

&& High[1]-Low[1]<900*Point

&& (High[3]-Low[3]>400*Point || (Close[4]<iBands(symbol,0,30,2,0,PRICE_MEDIAN,MODE_LOWER,4) && Close[5]<iBands(symbol,0,30,2,0,PRICE_MEDIAN,MODE_LOWER,5)))

&& Low[i]>Low[3] && Close[2]>iBands(symbol,0,30,2,0,PRICE_MEDIAN,MODE_LOWER,2)

&& Close[1]<iBands(symbol,0,30,2,0,PRICE_MEDIAN,MODE_LOWER,1)+20*Point

&& Low[1]<=iLow(symbol,0,iLowest(symbol,0,MODE_LOW,4,1))+20*Point

&& Low[1]<iBands(symbol,0,120,2,0,PRICE_MEDIAN,MODE_LOWER,1))

{

RemoveStopsandTargets();

open_price2 = NormalizeDouble(Bid, Digits);

stop_loss_price2 = NormalizeDouble(0,Digits);

take_profit_price2 = NormalizeDouble(0,Digits);

for (i = OrdersTotal() - 1; i >= 0; i--)

if (OrderSelect(i, SELECT_BY_POS))

if (OrderMagicNumber() == magic_number2) {

order_type = OrderType();

if (order_type == ORDER_TYPE_SELL) {

if ((NormalizeDouble(OrderOpenPrice(), Digits) != open_price2) || (NormalizeDouble(OrderStopLoss(), Digits) != stop_loss_price2) || (NormalizeDouble(OrderTakeProfit(), Digits) != take_profit_price2)) {

if (!OrderModify(OrderTicket(), open_price2, stop_loss_price2, take_profit_price2, OrderExpiration()))

Print("Error: ", ErrorDescription(_LastError));

}

break;

}

else if (order_type == ORDER_TYPE_SELL)

break;

}

if (i < 0)

if (OrderSend(symbol, OP_SELL, NormalizeDouble((nlongs-nshorts)*overhedge/100,2), open_price2, 3, stop_loss_price2, take_profit_price2, magic_number2+" EQUITY HEDGER SELL 0/0", magic_number2) < 0)

Print("Error: ", ErrorDescription(_LastError));

}

else

for (i = OrdersTotal() - 1; i >= 0; i--)

if (OrderSelect(i, SELECT_BY_POS))

if (OrderMagicNumber() == magic_number2)

if (OrderType() == ORDER_TYPE_SELL_STOP)

if (!OrderDelete(OrderTicket()))

Print("Error: ", ErrorDescription(_LastError));

return(0);

}

}

double RemoveStopsandTargets()

{

int i;

for (i = OrdersTotal() - 1; i >= 0; i--){

if( OrderSelect(i,SELECT_BY_POS, MODE_TRADES))

if( OrderType()==OP_BUYSTOP && MathAbs(OrderOpenPrice()-Ask)<.003)

OrderDelete( OrderTicket() );

else if( OrderType()==OP_SELLSTOP && MathAbs(OrderOpenPrice()-Bid)<.003)

OrderDelete(OrderTicket());}

for (i = OrdersTotal() - 1; i >= 0; i--){

if( OrderSelect(i,SELECT_BY_POS)){

if (OrderType() == OP_SELL

//&& OrderMagicNumber()!=magic_number3

){

if (!OrderModify(OrderTicket(), OrderOpenPrice(), NormalizeDouble(0,4), NormalizeDouble(0,4), OrderExpiration()))

Print("Error: ", ErrorDescription(_LastError));

}

if (OrderType() == OP_BUY

//&& OrderMagicNumber()!=magic_number3

) {

if (!OrderModify(OrderTicket(), OrderOpenPrice(), NormalizeDouble(0,4), NormalizeDouble(0,4), OrderExpiration()))

Print("Error: ", ErrorDescription(_LastError));

}

}

}

return(0);

}I am baffled by people who think they can trade everything. I am barely starting to develope some understanding for one single instrument’s behavior.