Dorime, Amme-mo.

Nick Rhodes has a plot for daily embedding, that it prints into the 2nd indicator window.

if (Period()==1440 && iStochastic(symbol,1440,18,3,3,MODE_SMA,0,MODE_SIGNAL,i+2)<24 && iStochastic(symbol,1440,18,3,3,MODE_SMA,0,MODE_SIGNAL,i+1)<24 && iStochastic(symbol,1440,18,3,3,MODE_SMA,0,MODE_SIGNAL,i)<24 ){

ObjectCreate("Fracabbb"+IntegerToString(i), OBJ_RECTANGLE, 2, Time[i+1], 24, Time[i], 0);

ObjectSetInteger(0,"Fracabbb"+IntegerToString(i),OBJPROP_COLOR,clrSalmon);

ObjectSet("Fracabbb"+IntegerToString(i),OBJPROP_BACK,1);

ObjectSet("Fracabbb"+IntegerToString(i),OBJPROP_WIDTH,5);

}

if (Period()==1440 && iStochastic(symbol,1440,18,3,3,MODE_SMA,0,MODE_SIGNAL,i+2)>78 && iStochastic(symbol,1440,18,3,3,MODE_SMA,0,MODE_SIGNAL,i+1)>78 && iStochastic(symbol,1440,18,3,3,MODE_SMA,0,MODE_SIGNAL,i)>78){

ObjectCreate("Fracabbbb"+IntegerToString(i), OBJ_RECTANGLE, 2, Time[i+1], 80, Time[i], 100);

ObjectSetInteger(0,"Fracabbbb"+IntegerToString(i),OBJPROP_COLOR,clrChartreuse);

ObjectSet("Fracabbbb"+IntegerToString(i),OBJPROP_BACK,1);

ObjectSet("Fracabbbb"+IntegerToString(i),OBJPROP_WIDTH,5);

}How this plot can be used to determine the age / current state of the swing?

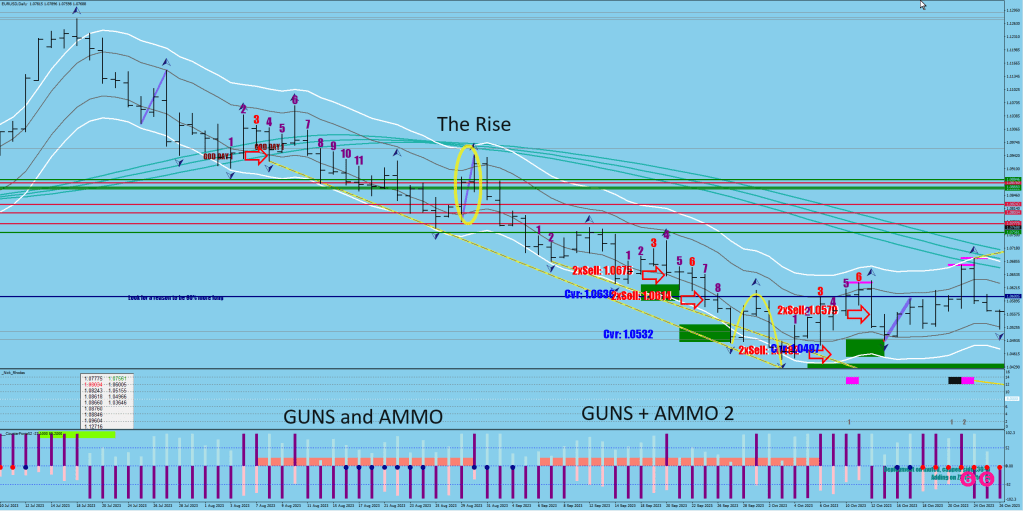

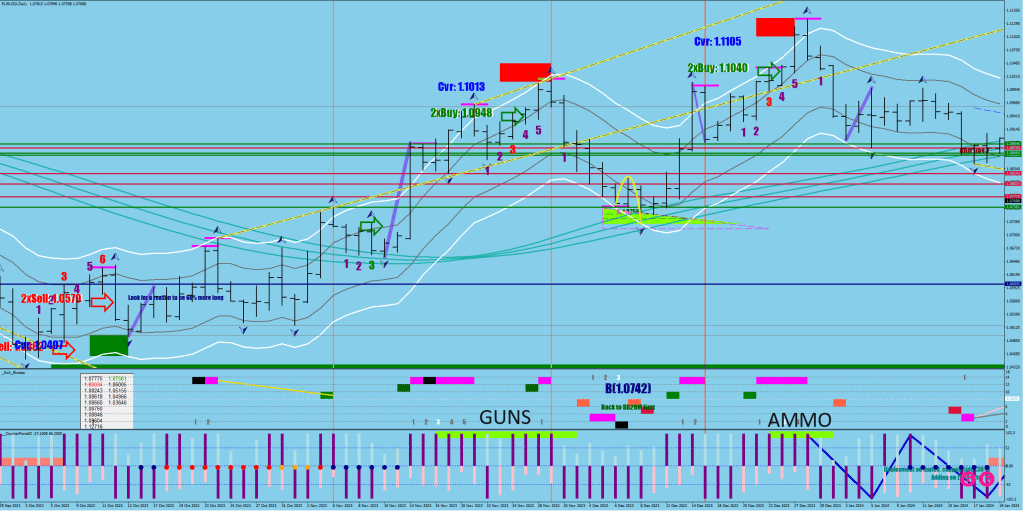

As the thesis goes, you need guns and ammo.

The first block is marking up the location of the guns found.

If the search goes on for 10 or more days, you may have some ammo found too.

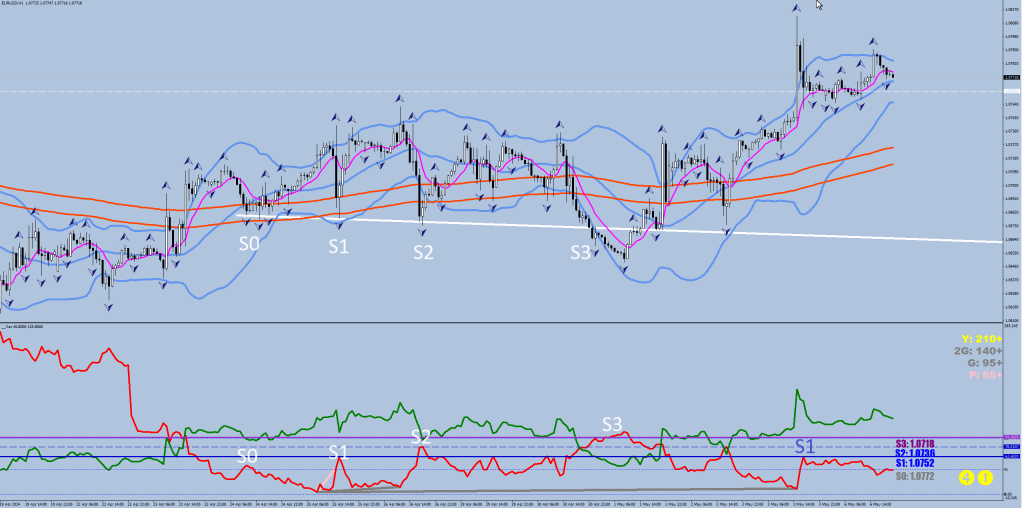

Examples.

The first image shows a 10-day stretch

Pay attention to the bow back that takes place in 6 days or less.

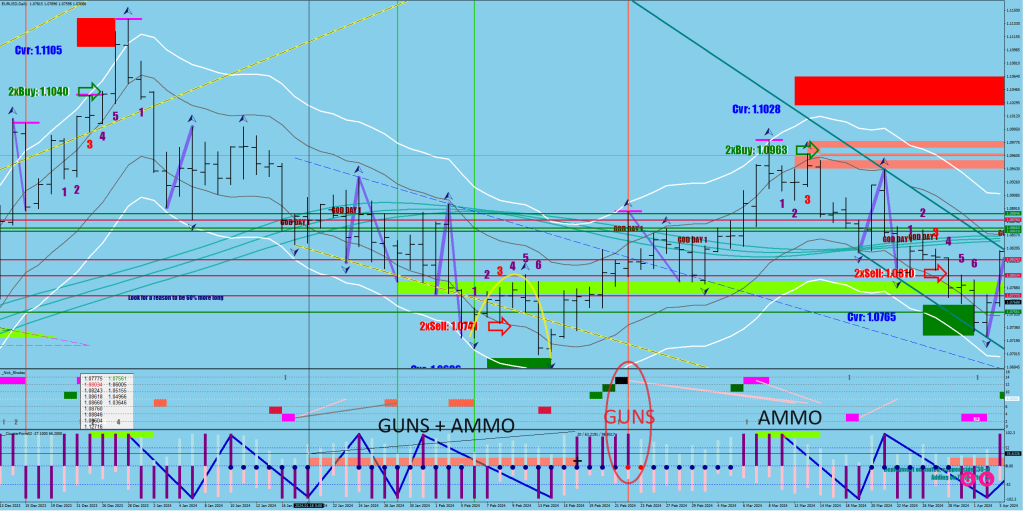

The second example is a Guns + Ammo 16-day search with a bow-back tail.

Of course, the Guns and Ammo blocks are completely separate.

Now we throw liquidity break in the mix. You don’t want to see a lack of buying / a quick lift after a phase of embedding.

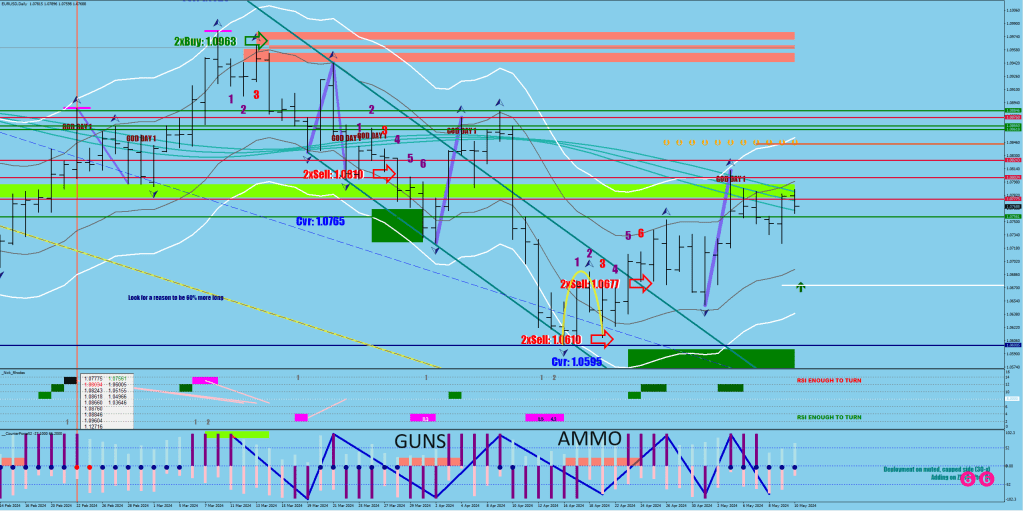

The next one had a deeper pullback in between with a 2-day bow back.

The followin is clearly a G+A with a 6-day bow back at the end.

The above has my one single example where Guns were found without Embedding. The combination of the strong squeeze (red ball on the histogram) and a black print (a slip with an extra high RSI2 print).

////upside black in the magenta sequence

else if (RSI2[i]>96 && High[i+1]<High[i+2]){

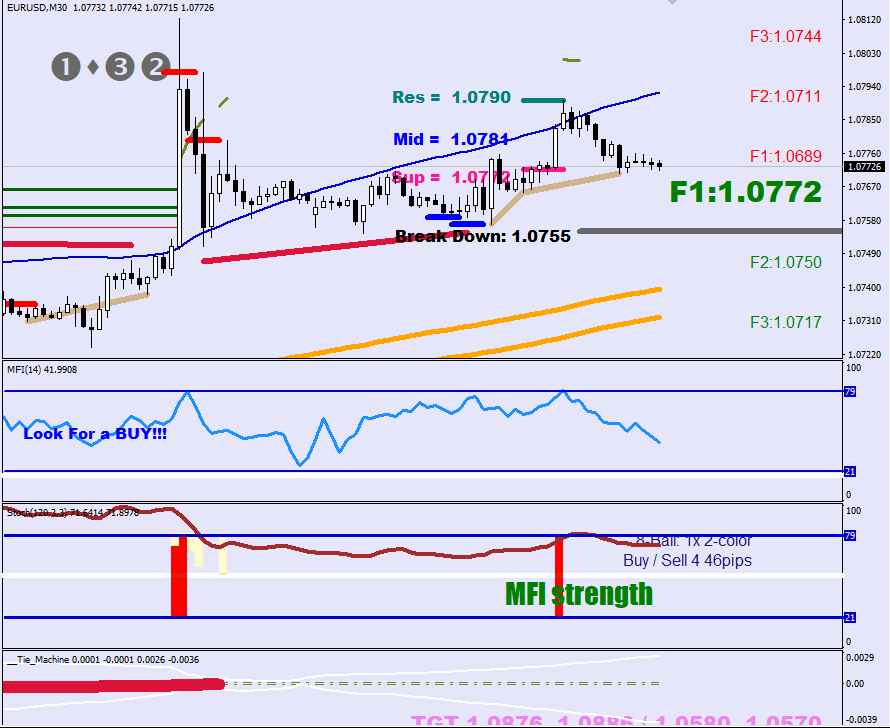

score[i]=3;Two things about the last one. The G+A down is clearly visible with the 3-day Bow. Yet, on the upside…

…there hasn’t even been a Guns print yet.

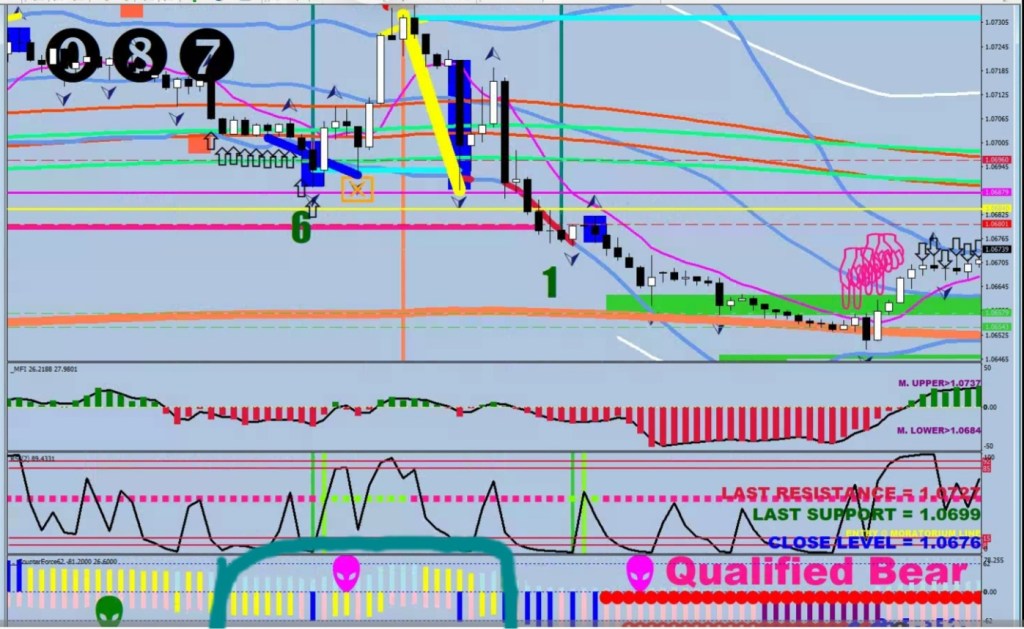

Nostalgia: I called the divergences Guns and Ammo already back in 2021

///// upper guns + ammo pink divergence

if (score[i]==0

&& score[i+1]<3

&& (score[i+1]>0 || (score[i+1]<score[iHighest(symbol,0,MODE_HIGH,16,i+6)] && upC[i+1]!=EMPTY_VALUE))

&& score[ArrayMaximum(score,12,i+6)]>2

&& High[i+1]>iHigh(symbol,0,iHighest(symbol,0,MODE_HIGH,12,i+6))

&& score[ArrayMaximum(score,12,i+6)]>score[ArrayMaximum(score,12,i+6)+1]

&& score[ArrayMinimum(score,12,i+6)]>-3

){

ObjectCreate("Panacean"+DoubleToStr(i), OBJ_TEXT, 0, Time[i+1], High[i+1]+70*Point);

ObjectSetText("Panacean"+DoubleToStr(i), "DVG DN", 12, "Impact", clrYellow);

ObjectSet("Panacean"+DoubleToStr(i), OBJPROP_BACK,1);

ObjectCreate("Divergence"+i,OBJ_TREND,indicator_window,Time[i+1],8+score[i+1]*2-1,Time[ArrayMaximum(score,20,i+6)],8+score[ArrayMaximum(score,20,i+6)]*2-1);

ObjectSetInteger(0,"Divergence"+i,OBJPROP_RAY_RIGHT,false);

ObjectSet("Divergence"+i,OBJPROP_COLOR,clrPink);

ObjectSet("Divergence"+i,OBJPROP_WIDTH,3);

ObjectSet("Divergence"+i,OBJPROP_BACK,1);

if (Close[i+1]<c0[0]){

ObjectCreate("Panaceattt"+DoubleToStr(i), OBJ_TEXT, 0, Time[i+1], High[i+1]+70*Point);

ObjectSetText("Panaceattt"+DoubleToStr(i), ",", 58, "Webdings", clrWhite);

ObjectSet("Panaceattt"+DoubleToStr(i), OBJPROP_BACK,1);

ObjectCreate("Panaceatt"+DoubleToStr(i), OBJ_TEXT, 0, Time[i+1], High[i+1]+70*Point);

ObjectSetText("Panaceatt"+DoubleToStr(i), ",", 52, "Webdings", clrMagenta);

ObjectSet("Panaceatt"+DoubleToStr(i), OBJPROP_BACK,1);

}

if (i<120 ){

ObjectCreate("Fracabb"+IntegerToString(i), OBJ_RECTANGLE, 0, Time[i+1], iHigh(symbol,0,i+1), Time[0], iHigh(symbol,0,i+1)+160*Point);

ObjectSetInteger(0,"Fracabb"+IntegerToString(i),OBJPROP_COLOR,clrSalmon);

ObjectSet("Fracabb"+IntegerToString(i),OBJPROP_BACK,1);

ObjectSet("Fracabb"+IntegerToString(i),OBJPROP_WIDTH,5);

}

}