What to concentrate on?

The Fractals

We have fractals thanks to Bill Williams.

They should limit the very things you need to concentrate on, yet they have awful limitations.

One limitation is the sample size: the iFractals routine would “advance” the Fractal to the last bar to the left of the current one yet the current read isn’t settled yet not to mention the one that is to be printed in the future. You can only can call something a fractal if it has two, bars to its right settled. In other words there is uncertainty to any fractal print that is less than 3 bars away from the last one. All calculations that disregard this fact may end up with false conclusions, bad triggers.

The other, even more problematic thing is the speed incompatibility. The market has different speeds, and sometimes it would move way faster then your chosen metric, your time frame.

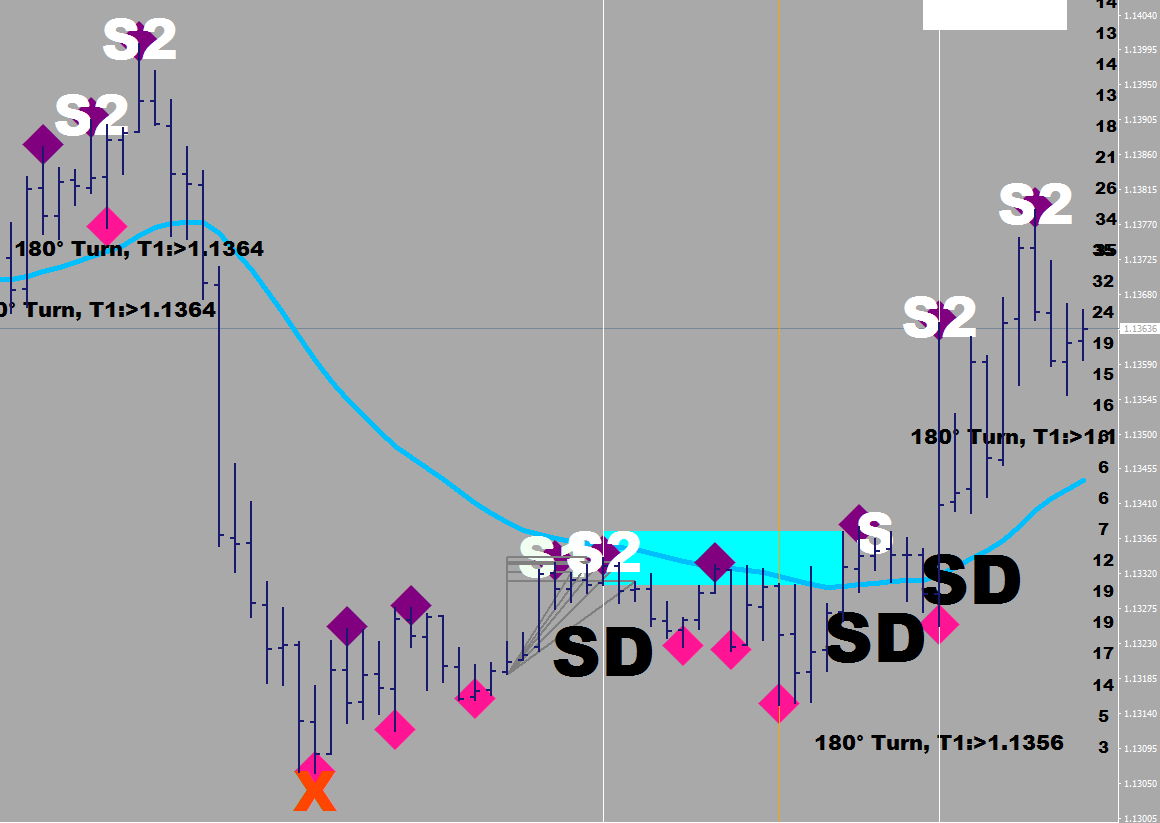

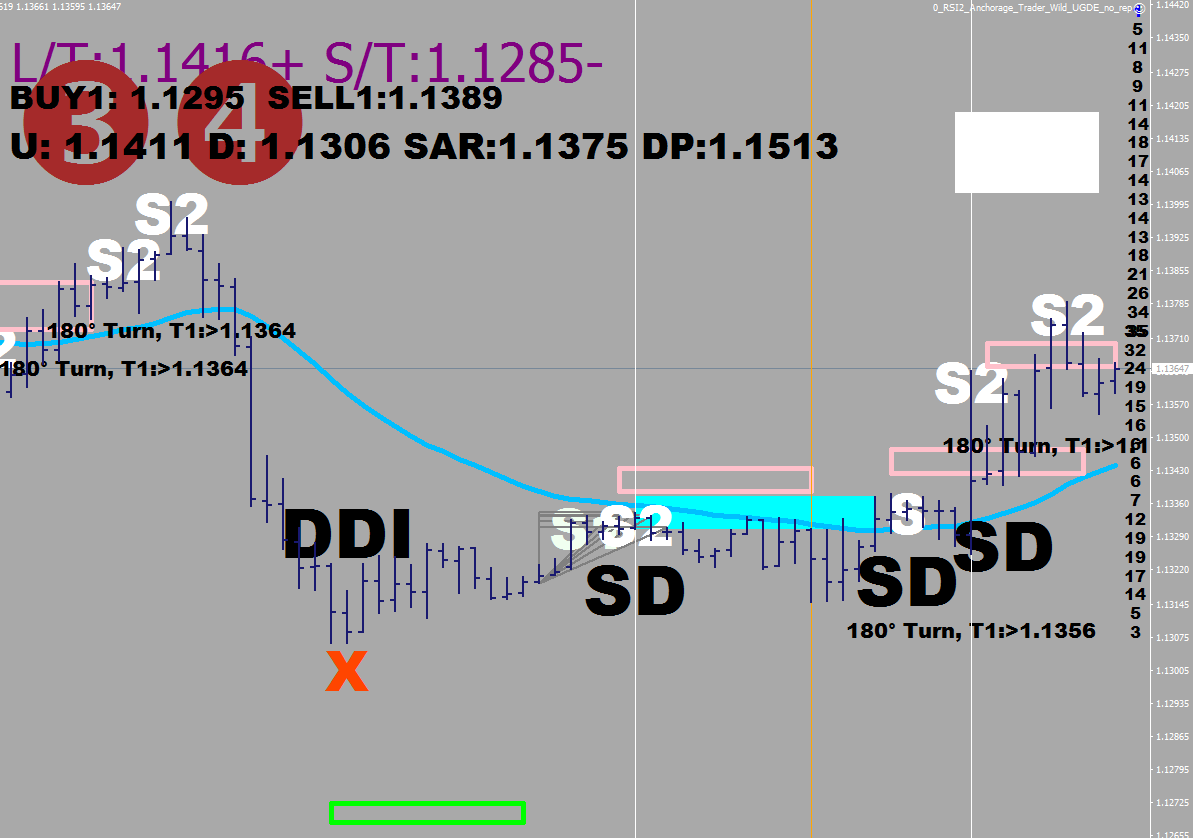

Take a look at the sell-off below. There is a down leg, that ends in that orange X.

It shows only 1 fractal (diamond). Were there no other fractals then? Yes, of course there were. You may have to go back down several time frames to make them appear. (You can see that the X fractal was actually a bottom tested twice.)

Why is this a problem? Because it throws off your fractal count. And you have no tangible measuring points for finding terminal length waves, especially if speed the market commutes at does not leave even a blip on the RSI2.

(Teminal length Waves in black)

Yet we want the fractals. But they are too many still. What if you started marking the ones that are both oversold/overbought on RSI2 and 9-sample Stochastic D as “Sync” lows and sync highs?

stoch[i]=iStochastic(NULL,0,9,3,3,MODE_SMA,1,MODE_SIGNAL,i);

RSI2[i]=iRSI(NULL,0,2,PRICE_MEDIAN,i);

if(stoch[i+1]<23 && RSI2[i+1]<16 && RSI2[i+3]>5 && !(stoch[i]<5 && RSI2[i]<5)&& iFractals(Symbol(),0,MODE_LOWER,i+1))

sdn[i+1]=Low[i+1];

if(stoch[i+1]<38 && RSI2[i+1]<16 && !(stoch[i]<5 && RSI2[i]<5)&& iFractals(Symbol(),0,MODE_LOWER,i+1))

sdn[i+1]=Low[i+1];

if(stoch[i+1]<44 && stoch[i+1]>5 && RSI2[i+1]>5 && !(stoch[i]>15 && RSI2[i]>15) && iFractals(Symbol(),0,MODE_LOWER,i+1))

sdn[i+1]=Low[i+1];

if(stoch[i+1]<5 && RSI2[i+1]<5 && !(stoch[i]>15 && RSI2[i]>15) && iFractals(Symbol(),0,MODE_LOWER,i+1))

sdn[i+1]=Low[i+1];

if( ((stoch[i+1]>64 && stoch[i]<85 && RSI2[i+2]>85 ) || (stoch[i+1]>72 && stoch[i+1]<75 ) || (stoch[i]>44 && stoch[i+1]<35 && stoch[i-1]<44 && RSI2[i+1]>85 )) && RSI2[i+1]>70 && !(stoch[i-1]>95 && RSI2[i-1]>95) && ( iFractals(Symbol(),0,MODE_UPPER,i+1) ) && !sup[i+2] )

sup[i+1]=High[i+1];

if(stoch[i+1]>64 && stoch[i+2]<64 && RSI2[i+1]>85 && !(stoch[i]>70 && RSI2[i]>95) && ( iFractals(Symbol(),0,MODE_UPPER,i+2) ) && !sup[i+2] )

sup[i+1]=High[i+1];

if(stoch[i+1]>85 && RSI2[i+1]>85 && !(stoch[i]>85 && RSI2[i]>95) && iFractals(Symbol(),0,MODE_UPPER,i+1) && !sup[i+2] )

sup[i+1]=High[i+1];

I have a sorting routine that names them further as S, S1 or S2 and X. No two brokers data would be the same, but you are only going to start to find out how different they really are, when you start plotting with multiple ones at the same time. One broker may call a bar a doji, for they never adjusted the bid during the period while the other made a transaction and has a bar that has a body. Imagine if you are looking for 3 green candles as a sequence. One broker would find it, the other (with the doji) would not, for a doji’s close may not be higher than its open.

Since the bid data isn’t the same, the RSI, derived values would not be the same either. One thing I had to personally do to synchronize the end result between two brokers when plotting the Forest, was to use different cross back values: one broker’s RSI 77.8 is the other broker’s 77.7 – that one tenth can make all the difference at times.

Since this article is getting lengthy, I’m only going to discuss the surprise turn that happened today, and two ways that you could had spotted it.

Concentrate on the cyan shading please. It is the time out resistance that was made within 8 hours of the first thrust up. The high of the box was taken out – which should not have happened, and price then trickled down to the E-16.

The main lesson for you in this, “what to concentrate on” section is the idea of relativity and the significance of the seemingly insignificant.

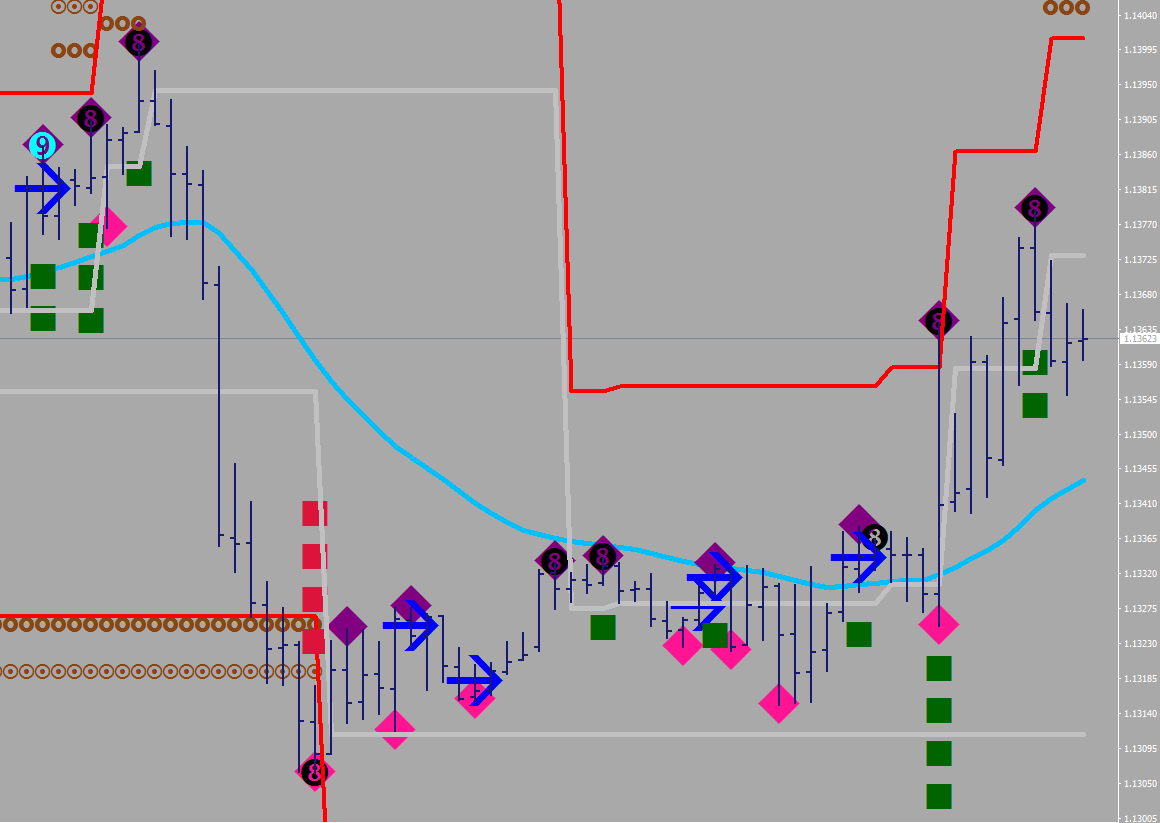

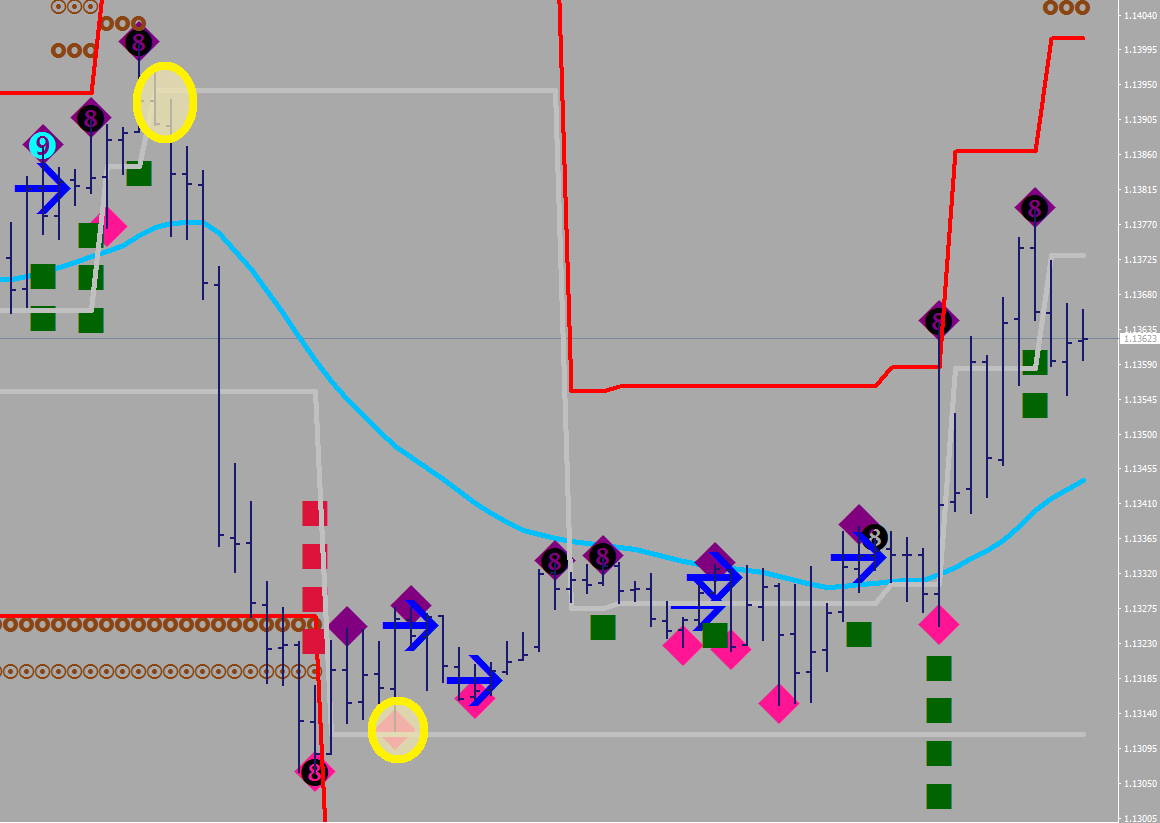

On the image below, please tell me what is the most important occurrence, the most precise telltale of the dynamics?

I’ll help a little.

What happened under the first yellow-out? The market lost the overbought status.

What happened under the second? The market back tested the oversold level.

The sliver lines on the gray background – ironically are the best visuals to tell you about the consolidation. The qualifying run, the first “Sync” fractal adjusted the overbought level lower. All the consolidation was taking place around the overbought line and the oversold line was never touched again.

The gray plots as well as the time out boxes are part of my 88 Luftballons routine.

The calculation for the gray lines:

if (sdn[i+1]!=0) {minus9[i]=Low[i+1]-110*Point; minus[i]=minus9[i]+FSize/2*10*Point; minus15[i]=Low[i+1]-180*Point; minus22[i]=Low[i+1]-240*Point;}

if (sup[i+1]!=0) {plus9[i]=High[i+1]+100*Point; plus[i]=plus9[i]-FSize/2*10*Point; plus15[i]=High[i+1]+170*Point; plus22[i]=High[i+1]+220*Point;}

where FSize is 32 as per EUR/USD, and the gray lines are the plus and the minus