The show down of the titans.

First the findings.

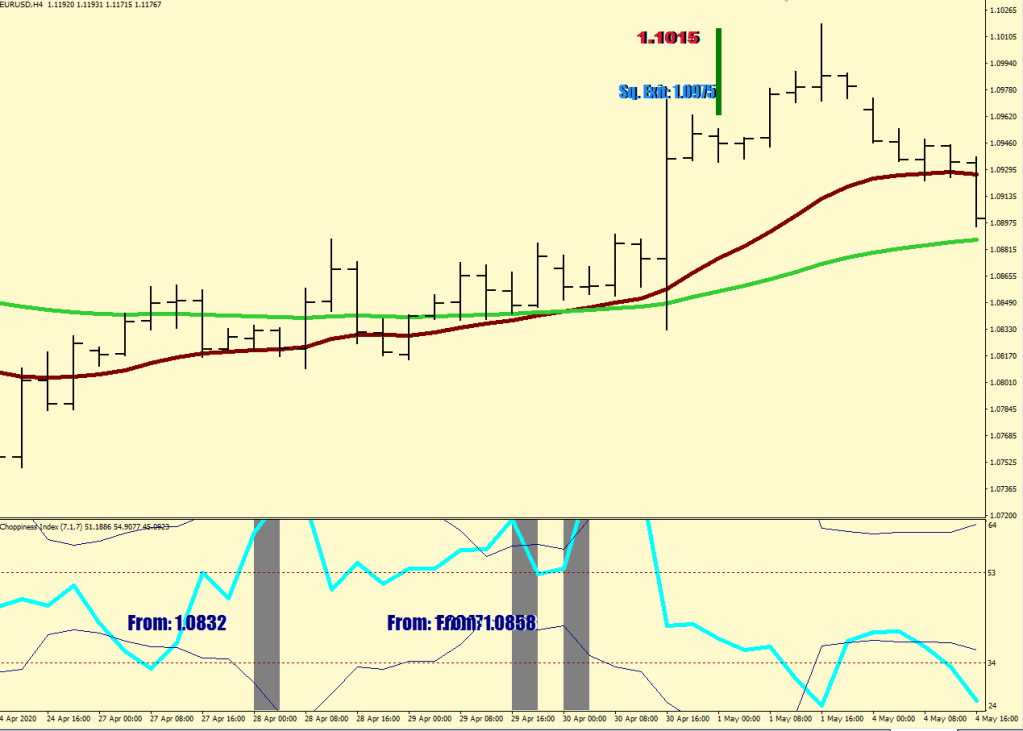

I marked up in gray abrupt bursts above 59 CI and reaches over 65 CI (7–sample).

(ChoppinessIndex(7,i)>65 && ChoppinessIndex(7,i+1)<65) || (ChoppinessIndex(7,i)<59 && ChoppinessIndex(7,i+1)>59 && ChoppinessIndex(7,i+2)<59 && (ChoppinessIndex(7,i+3)>54 || ChoppinessIndex(7,i+2)<50))I also plotted the by now filtered extension projections, but the basic idea is still having a qualified move (large enough during a time limit) pointing to 50% more to be accomplished further down the road.

iHigh(NULL,240,i+3)-iLow(NULL,240,i+1)>FSize*26*Point && iLow(NULL,240,i+1)<iLow(NULL,240,i+3) && iLow(NULL,240,i+1)-(iHigh(NULL,240,i+3)-iLow(NULL,240,i+1))*.5The last change I made was changing the ATR filter to a fixed size measurement.

Now, the images & the conclusions.

Enter with a size that can bear draw down of 60 pips. At 60 pips draw down from the consolidation level (Enter) if price went against you, hedge. At 70-pips you double the size of the counter holdings. You hold them into the next extension fill, where you scale out. You take off the original holding 40 pips back from the extension fill level (see article about Squaring).

Yea, that’s all I’ve got right now.

bonus image 1

bonus image 2

bonus image 3