One thing led to another. I saw this video yesterday>

Since recently I volunteered myself into a challenge of making 1000% gains in a single year, I was thinking: this is the ice bucket!

Beating the game and retiring early are not major challenges. Beating Kevin is. He claims to have a portfolio equity of $8 million ($17 million minus $9 million mortgage) plus $9 million in stocks. He started with cca $19k in 2009, and so 12 years is the time limit to beat him. Only cash, securities and equity would count, not net worth derived from yearly gross business revenue multiplied by 10.

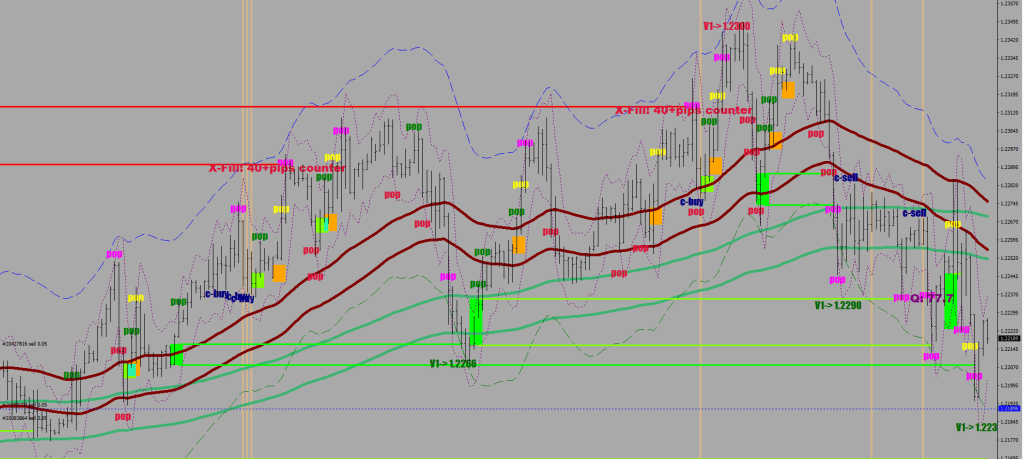

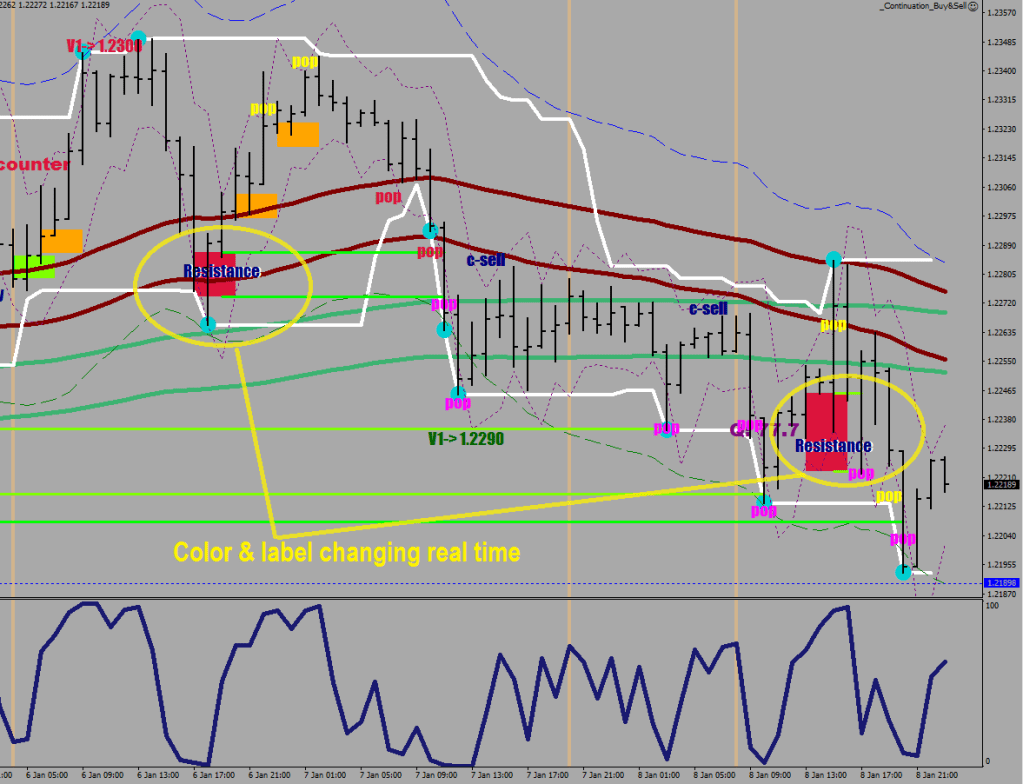

So I was to leave for my shift (can’t work from home), and in the last few minutes at home still, upon realizing that I was missing out on 2 continuation sells, I made plots for them (there is a continuation buy as well on the left):

This of course used to cost me fractal-search recursions, but today I opted for ArrayMaximum / ArrayMinimum. The realization that these functions may be returning the index of the array, not the value was sobering.

if (RSI2[ArrayMaximum(RSI2,16,i)]==RSI2[i] && iHigh(symbol,60,iHighest(symbol,60,MODE_HIGH,15,i+1))>High[i] && RSI2[i]<75)

I had no time to make my green tea.

Sitting on the Central Line I was staring at the non-moving screen somewhere between Infe Station and Mole Station. I figured I should automatize these trades.

After I got to work, I grabbed my work tablet and started coding remotely. It is rather slow trying to copy-paste things from a distance, but I had the new cropper inserts and the Continuation Buy & Sell ea ready and running on my system at home less than 30 minutes.

By utilizing the stop loss value as a code as well as the target, I can now call upon two different croppers at the same time: I can have a close below an RSI reading as well as below a Stochastic reading or at a distance from a moving average – whichever comes first.

From here on the continuation trades would happen automatically (in & out), regardless of me being underground or without coverage or sleeping shamelessly.

Of course, my denominator would not be “1 professor of trading” if I did not make the necessary, elegant changes for sustainability.

if (nlongs==0) shortsz = NormalizeDouble((MaxLots-nshorts),2);

else shortsz = NormalizeDouble((nlongs-nshorts),2);

if (shortsz>MarketInfo(symbol,MODE_MAXLOT)) shortsz=MarketInfo(symbol,MODE_MAXLOT);

I opted out from overhedging, consulted with the broker for maximum lot size, and even cranked down the size to

double MaxLots = NormalizeDouble(AccountEquity()/2/1000,2);

which I now refer to as Trading Size (T/S), not Full Size (F/S).

Honestly, I would only need a handful of these fluent solutions and I would gain the confidence to nominate myself.